1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

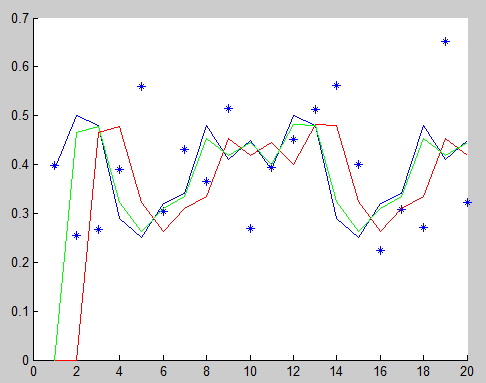

| %% Adaptive Kalman filter

clear all;clc;format short;

z=[0.39, 0.5, 0.48, 0.29, 0.25, 0.32, 0.34, 0.48, 0.41, 0.45,0.39, 0.5, 0.48, 0.29, 0.25, 0.32, 0.34, 0.48, 0.41, 0.45];

%% First Order Adaptive Kalman Filter

x_inter=zeros(1,20);

x_current=zeros(1,20);

P_current=1;

Q=0.382;

q_t=0.1;

R=0.1;

A=1;

B=1;

u=0;

for t=2:20

% **************Predict**************

x_inter(t)=A*x_current(t-1)+B*u;

P_inter=P_current+Q;

% **************Update**************

K=P_inter/((P_inter+R));

x_current(t)=x_inter(t)+K*(z(t)-x_inter(t));

%x_current(t)=(1-K)*x_inter(t)+K*A(t)+(1-K)*q_t;

P_current=(1-K)*P_inter;

end

real_value=z

estimated=x_current

mse = (sum(x_current.^2))/20

figure();

hold on;

plot(z,'b');

plot(x_inter,'r');

plot(x_current,'g');

hold off; |

Répondre avec citation

Répondre avec citation

Partager